The ISM Services PMI increased to 53.5% in February…Improving from 52.8% in January.

What does it mean – Expansion in the nation’s largest sector accelerated in February. This takes a little edge off the market’s growth concerns but will do little to dampen the noise.

Retail sales increased 0.2% month-over-month in February…following a downwardly revised 1.2% decline (from -0.9%) in January.

What does it mean – Excluding autos, retail sales were up 0.3% month-over-month. Non-store retailer sales jumped 2.4% month-over-month.

The February CPI report came in softer than expected…Coming in at .22 vs. the consensus of .3.

What does it mean – While down nicely, inflation is still sticking above the Fed’s 2.0% target.

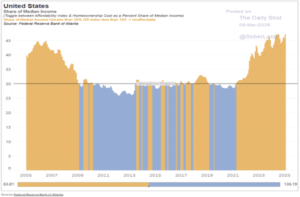

Homeownership cost near all-time highs…As a share of median income, US housing affordability has been deteriorating.

What does it mean – If history rhymes, or repeats, housing could be in trouble. According to the Atlanta Fed, the numbers are reminiscent of 2006. Take a look at the following chart.

Your mortgage is much more than your interest and principal…Here is the breakdown of homeownership cost for the average home buyer.

What does it mean – While principal and interest make up the biggest part of one’s payment, property taxes have skyrocketed due to the massive increase in property values and with that so has insurance costs. According to the Atlanta Fed the average monthly cost to own a home in the U.S. is now over $3,100 up from just over $1,600 in 2020.

Income needed for homeownership…The cost of home ownership as a percent of annual income has exploded to record highs.

What does it mean – Historically banks lent 30% on a borrower’s annual income. With interest rates at record lows banks began to ease the lending requirements and, in many cases, will lend up to 40% + of income and more in some cases.

When it comes to conforming loans, the banks take literally no risk, as most conforming loans are Freddie Mac and Fannie Mae loans. These are GSE’s or Government sponsored Enterprises that operate in the free market with the explicit backing of the government. Hmm…Don’t worry there is nothing wrong with this.

With the back stop of the Federal Government, also known as you, the taxpayer, another government agency better known as Ginnie Mae or the Government National Mortgage Association purchases conforming loans to create capital for Fannie Mae and Freddie Mac to originate more loans backed by you, the taxpayer.

Don’t get me wrong, we have all benefited from easy money, low interest rates and the government derisking the lender from responsibility to make sure the borrower could actually pay the loan. Heck, all of our homes have doubled in the last few years and property values are up 4x in parts of the country over what they were 30 years ago. In essence the government derisked the banks by fooling you, the taxpayer, and tempting you with greed and the wealth creation of home ownership. Remember last week’s letter about Odysseus and the Sirens and the risk of temptation and the importance of self-control.

Today, the U.S. median income is roughly $80,000. Yet, to purchase the average family home at today’s current price by financing 80%, pay the taxes, and insurance you will need to make over $120,000 a year.

Due to massive printing of money and the explosion of government, we have inflated our way out of the American Dream for many Americans and most of our children.

Treasury deficit continues to expand…Congress better get on board and wake up. The Treasury Budget for February showed a deficit of $307.0 billion compared to a deficit of $296.3 billion in the same period a year ago based on the Continuing Resolution pushed through Congress prior to the election in Nov. 2024.

What does it mean – While Congress has spent the last 50 years confusing congressional hearings with actual work of real oversight, the Treasury budget is running amuck with waste, fraud, abuse, and incompetence. Expect this to continue until an actual budget is passed.

Now that DOGE is shedding light on waste, fraud, abuse, and incompetence, one has to ask, when will Congress actually ask each Agency what they really need to run their departments and actually budget towards reality instead of guesstimating with your hard earned money.

Eggflation… Stop killing the chickens. Over the last few years the U.S. stopped listening to the farmers and relied on the academics to oversee the bird flu creating massive shortages. With a quick shift in policy, the cost of eggs has dropped over 10% since beginning of the year.

What does it mean – Policy matters. While Bird Flu has been around for some time. How we handled it has changed. The U.S. applies the “stamping out policy”. Per the FDA contagious viruses are to be stamped out by killing the entire flock or heard.

U.S. farmers are required to kill their entire flock. Over 160 million chickens have been destroyed over thew last few months, creating a shortage in the U.S. while other countries listened to the experts – the Farmer. Many other countries have had no issues as they separated the infected birds from the flock and culled or destroyed only the sick birds. These countries saw their egg prices level out at prices ranging from an equivalent cost of roughly $2.65 per dozen and under $2 in many parts of the world, while we in CA have consistently suffered under prices ranging between $7 and $9 per dozen and in some areas up to $12.00 during this same time period and across the U.S eggs have hovered between $5 and $8 a dozen. During COVID, these are the very same “experts” that shut down our schools, churches, and encouraged businesses to let folks work form home and mandated vaccines to children that had a 99.999% survivability rate.

With farmers becoming more proactive, the cost of eggs in the US decreased 0.63 USD/DOZEN or 10.88% since the beginning of 2025, according to trading on a contract for difference (CFD) that tracks the benchmark market for this commodity. Historically, Eggs in the U.S. reached an all-time high of 8.17 in March of 2025.

The Biggest Story no one is talking about!!

The next Gold Rush…Utah HB306 passed. Since Friday March 7, 2025, a day that will one day prove to be the most important day in economic history since the US went off the Gold Standard.

In fact, I cannot get out of my head the song “I am so excited” by the Pointer Sisters. As Americans we should be jumping for joy. Unleashing our celebratory instincts unless you are prone to burning down your city after your professional team wins a championship. But that is what Utah has given us all. A reason to celebrate!!! Putting the people, the individual back in charge of their economic future.

The United States Constitution states in Article I, Section 10, “No State shall…make any Thing but gold and silver Coin a Tender in Payment of Debts.” Utah, I am so excited, I just can’t hide it.

What does it mean – We are one step closer to having an option as individuals to utilize gold and silver as a currency. Last week, the Utah House and Senate gave final approval to a bill that would create a system allowing the state to make and accept payments in gold and silver. The payment system would use “gold or silver vaulted within the state,” be made publicly available, and allow for “the redemption of physical gold or silver by system participants.”

Can you Imagine?

Can you imagine, millions of Americans opting out of a fiat currency (digital or paper) and having the choice to use transactional gold to receive payments and pay bills. No longer being hit with a capital gains tax.

Let’s dream a bit…The U.S. median income is roughly $80,000 per year. There are over 163 million people employed. Based on the median salary times the number of employed Americans, total salaries paid out is over $13 trillion. According to historical numbers, that is roughly the value of gold in Fort Knox based on the last audit done nearly 50 years ago.

Think about this. What would the price of gold be if one-third or roughly 54 million people utilized transactional gold to pay their bills? What would it mean to the Federal Reserve?

Simply put, if you had a choice to take your paycheck in gold and utilize it to pay your bills, your checking account alone would outperform money markets and typical savings accounts and historically perform far better than the bond market and in some years in line or even better than the S&P500. Vastly improving one’s lifestyle and putting you in control of your financial future. Your lifestyle will improve far beyond a 3% increase in your salary every year.

Fiat currency – The Reality of the dollar.

The definition of fiat currency is a government currency not backed by anything tangible like gold or silver.

In 1971 the U.S. officially went off the Gold Standard at a price of roughly $44.60 per ounce. Today, gold stands at $2,994 an ounce and the $1 has lost 88% of its purchasing power since 1971 per the charts below. Adjusted for inflation it would take $7.84 to purchase the same item in 1971 for $1.00. Folks, that is inflation due to the printing press. Yet, the Fed believes 2% inflation is good. One must ask why. It certainly won’t help the consumer or the saver. See below.

When comparing the purchasing power of Gold today vs. 1971 the numbers are staggering.

According to HUD, The Department of Urban Development, the average home price in the USA in 1971 was $25,200. Gold was at $44.60 per ounce. If we purchased a home in 1971 when the dollar was backed by gold, it would have cost the average home buyer 565.02 ounces of gold.

The average home in the USA at the end of 2024 was $419,200. With Gold at $2,994 an ounce, we could have purchased 4 homes with the 565.02 ounces of Gold or had a value of $1,691,669.88.

After going off the gold standard in 1971, our country suffered massive inflation both times when the Fed initiated a loose money policy and printed money to spark consumption.

Since 2001 and specifically from 2006 to present, the US economy has been artificially boosted in recent years by massive deficits and a very loose monetary policy. Directly causing massive inflation and weakening of the dollar.

Reversing course and reducing this artificial stimulus will be like having morphine wear off or a toddler coming off a sugar high. Brian Wesbury says it best, “what is good for the long-term makes the short-term look worse.” Looking back at history, this is much like what happened with Ronald Reagan in the early 1980s. Even though his policies led to a boom in the economy, the fix (especially for inflation) was a painful process.

Take a look at my good friend Kevin Freeman’s book Pirate Money. Nearly two-dozen states are already working on legislation to follow in Utah’s footsteps.

If Utah and these other states are successful in creating transactional gold, get ready for another gold rush.

Let’s roll America!!

Doug De Groote, CFP®, MBA, CTC

Managing Director

![]()

De Groote Financial Group, LLC is a federally registered investment adviser that maintains a principal office in the State of California. The information contained in this message is confidential, protected from disclosure and may be legally privileged. If the reader of this message is not the intended recipient or an employee or agent responsible for delivering this message to the intended recipient, you are hereby notified that any disclosure, distribution, copying, or any action taken or action omitted in reliance on it, is strictly prohibited and may be unlawful. If you have received this communication in error, please notify us immediately by replying to this message and destroy the material in its entirety, whether in electronic or hard copy format.